Capital flowed from emerging markets as pandemic, economic cycle took hold

J. Scott Davis and Andrei Zlate

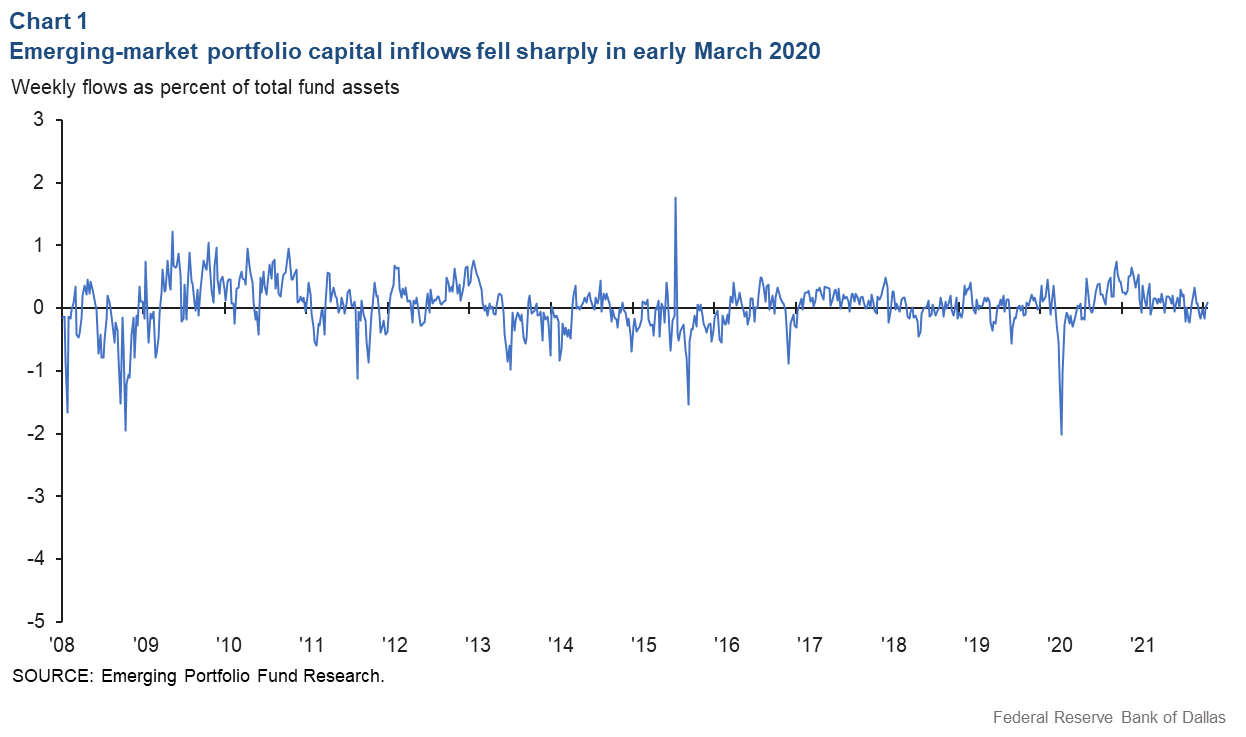

Weekly portfolio capital inflows to emerging-marketplace economies fell sharply as the COVID-19 pandemic shook the international economy in March 2020.

The fall was comparable to that throughout the depths of the World wide Economic Crisis in 2008, based on knowledge for a sample of 24 emerging-current market economies compiled by Rising Portfolio Fund Analysis and made use of here as a proxy for capital flows (Chart 1). The information present movement into emerging-sector bond and fairness mutual resources and trade-traded money (ETFs). In the 3rd 7 days of March 2020 and in the second 7 days of October 2008, weekly portfolio outflows from rising-industry resources totaled practically 2 percent of the funds’ complete property beneath management.

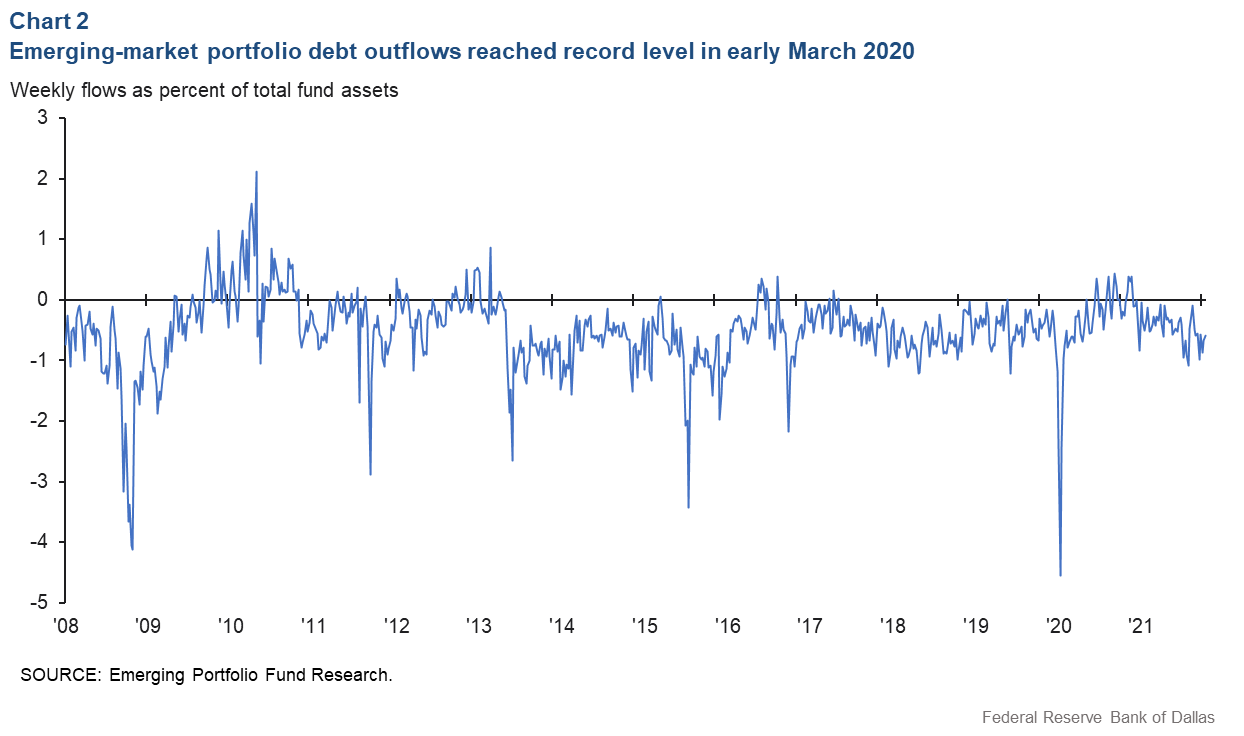

This pace of funds outflows is even far more extraordinary when focusing on portfolio personal debt flows—that is, outflows from emerging-current market bond money. The weekly speed of bond fund outflows in March 2020 was more than 4.5 {d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} of total belongings (Chart 2). That exceeded the speed from preceding crisis episodes of the past 15 years—the Worldwide Financial Crisis, the 2011 euro-area crisis, the 2013 “taper tantrum” and the 2015 Chinese renminbi devaluation.

Cycles in intercontinental funds flows are inclined to observe the cycles in world risky-asset costs, commonly referred to as the global money cycle. In a new Dallas Fed working paper, we find that fluctuations in the global financial cycle, reflecting impacts from the COVID crisis, account for approximately a single-3rd of the movement in rising-market inflows throughout 2020–23.

We get there at this conclusion by analyzing world-wide dangerous-asset charges and money flows close to the COVID disaster and asking three inquiries:

- How did the worldwide money cycle behave during the COVID crisis?

- What functions of an economy built it vulnerable to a sharp fall in funds inflows all through the COVID crisis?

- How well do fluctuations in the world monetary cycle describe cash flows during the COVID disaster?

Worldwide monetary cycle accompanied COVID disaster

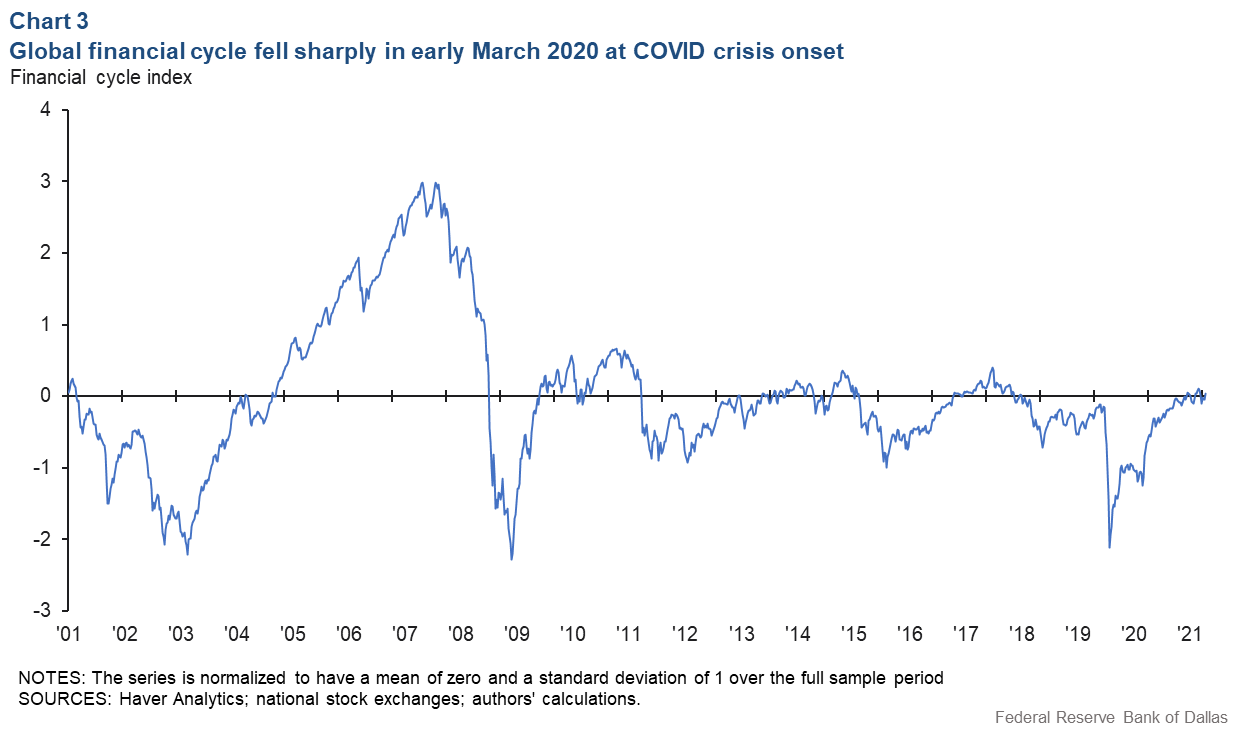

Silvia Miranda-Agrippino and Hèléne Rey (“U.S. financial coverage and the world-wide monetary cycle”) evaluate the world-wide financial cycle as the frequent trend in a panel of world risky-asset price ranges. These authors see this typical element at a month-to-month frequency, which for most analysis thoughts is additional than suitable. Nevertheless, to measure the world money cycle close to the COVID crisis, we extract a typical trend from a panel of stock marketplace indexes in 52 nations at a weekly frequency.

Chart 3 presents this weekly world monetary-cycle index, which is normalized to have a imply of zero and a normal deviation of 1 (that means the area exactly where around two-thirds of readings drop). We notice a two-normal-deviation fall (encompassing around 95 percent of results) in this prevalent part of global risky-asset rates over a four-7 days period from mid-February to mid-March 2020.

All through our over-all sample period of time, which starts in 2001, the only comparable world wide risky-asset price tag drop in magnitude and velocity was a two-regular-deviation index decrease about an 8-7 days period of time in September and October 2008 (the midst of the World-wide Fiscal Crisis).

Wanting at risky-asset rate details considerably less commonly would combine the crash in the global financial-cycle index in early March 2020 with a partial restoration that started out later on that identical month. When making use of the very same dangerous-asset price tag information aggregated at a monthly frequency, we observe only a 1.5 standard-deviation drop in the international economic cycle over February and March 2020.

A country’s vulnerability to a money inflows drop

We are notably interested to discover how a great deal a country’s portfolio funds inflows drop immediately after international risky-asset selling prices decrease. To find out this, we regress the weekly adjust in a country’s portfolio capital inflows on the weekly change in the world money-cycle index to estimate the elasticity, or sensitivity, of a country’s funds flows with regard to fluctuations in the international economic cycle.

We uncover that, on regular, weekly outflows from rising-marketplace debt or equity resources were about 2 p.c of full assets in reaction to a 1-regular-deviation fall in the international monetary-cycle index. This figure was about 2.5 p.c when concentrating on outflows from personal debt resources. These estimates are constant with the data introduced earlier detailing the sizable slide in rising-market portfolio flows and debt flows in response to the two-typical-deviation tumble in the worldwide economical-cycle index at the onset of the COVID crisis.

Our regression evaluation also highlights crucial cross-country distinctions in the sensitivity of a country’s capital inflows to fluctuations in the worldwide fiscal cycle. We locate, in line with other scientific studies, that macroeconomic factors these as a country’s present account equilibrium (complete of acquired and marketed merchandise, products and services and economic transactions) or a country’s web international-asset situation largely influenced how a country’s cash inflows responded to a downturn in world risky-asset charges.

All else equivalent, an raise in the ratio of the latest account to GDP of 1 share stage lowers the elasticity of a country’s total portfolio inflows by about .04 percentage factors of overall property. (A beneficial existing account suggests a country tends to make extra than it expends a adverse a single signifies the country expends a lot more than it requires in.)

In other words and phrases, evaluating a region with a current account deficit of 5 p.c of GDP and one with a recent account surplus of 5 {d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} of GDP, the portfolio funds inflows would be about .4 share details reduce in the deficit region in reaction to a a person-conventional-deviation slide in the international financial cycle.

Furthermore, this reaction would be .8 proportion details better next the two-common-deviation slide in the world-wide financial-cycle index at the onset of the COVID disaster. In the context of ordinary portfolio outflows of 2 p.c at the start of the COVID crisis proven in Chart 1, our estimates propose that cross-nation variances in the current account harmony clarify a considerable portion of the discrepancies in money flow responses.

The heterogeneity in funds movement responses appears even much more sizeable when focusing on portfolio debt flows. All else equivalent, an enhance in the current-account-to-GDP ratio of 1 percentage level lowers the elasticity of a country’s portfolio debt inflows by about .09 percentage points of full assets. Evaluating a nation with a present-day account deficit of 5 per cent of GDP and 1 with a latest account surplus of 5 p.c of GDP, portfolio personal debt outflows would be about 1.8 share details better in the current-account-deficit state at the onset of the COVID crisis.

While the effect of macroeconomic fundamentals these as present account balances on a country’s money outflows has been properly-documented, we also talk to if measures capturing the intensity of the COVID pandemic—like the weekly adjustments in new COVID conditions normalized by population—affect the reaction of a country’s portfolio funds inflows to a drop in the world wide money-cycle index.

We estimate that, all else equal, a doubling of the weekly new COVID cases—common at the starting of new an infection waves—raises the elasticity of a country’s complete portfolio inflows by .5 percentage details of full property. In other words, all else equivalent, at the world-wide onset of the COVID crisis in March 2020, a nation whose an infection counts were doubling each individual week would see a 1 proportion-level bigger drop in money inflows than a region exactly where COVID case counts remained stable.

Offered that the world money-cycle index fell by two typical deviations at the onset of the COVID crisis, immediate increases in COVID instances show up to have had a related effect as a big latest account deficit on cash inflows to a provided emerging-current market economic system.

Monetary-cycle fluctuations’ effect on portfolio funds inflows

Finally, we can request how properly fluctuations in the world-wide monetary cycle clarify the portfolio money inflows to rising markets, and if this marriage altered in the course of the COVID crisis.

We estimate the goodness-of-fit from our regression design. When regressing the weekly adjust in portfolio inflows on its possess lags and country-mounted effects—but without the need of the international financial-cycle element above our entire 2001–21 sample period—the goodness-of-in shape is about .20. In other text, lags and fastened outcomes alone can clarify about 20 percent of the fluctuations in the weekly change in rising-market portfolio capital inflows.

But when the world wide monetary-cycle aspect is included to this regression, the goodness-of-fit jumps to .45. Thus, the international money cycle explains approximately a fourth of the fluctuations in emerging-sector portfolio money inflows above our total sample.

The quantitative relevance of the global money cycle in conveying fluctuations in portfolio funds inflows is even higher around the last two many years of our sample time period, 2020–21. When incorporating the world wide monetary-cycle variable as an explanatory variable, the goodness-of-healthy of the design will increase from .17 to .50. As a result, the international economic cycle clarifies approximately a person-3rd of fluctuations in emerging-market place portfolio capital inflows through past two a long time in our sample that encompasses the COVID crisis.

About the Authors

The views expressed are all those of the authors and must not be attributed to the Federal Reserve Financial institution of Dallas or the Federal Reserve Method.