HBT Financial (HBT): My Top Bank For 2023, New Addition To Buy-And-Hold Bank Portfolio

yorkfoto/iStock by way of Getty Photos

HBT Monetary

HBT Money, Inc. (NASDAQ:HBT) bought on my radar in the third quarter when I determined financial institutions ideal positioned for mounting desire rates. I protected some of this research with Looking for Alpha viewers in an post entitled, “Have and Have Not Financial institutions.”

HBT is an less than-recognized and an less than-appreciated “Have Lender.”

This posting will do two points.

Initially, it features a “huge image” check out of Little- and Mid-Cap bank sector valuation knowledge. It exhibits that the sector is inexpensive in comparison to heritage. And, in the previous, comparable valuations have demonstrated to a favorable time for prolonged-time period buyers to develop positions in Superior-High-quality Modest- and Mid-Cap financial institutions.

Next, it describes why I have additional HBT to my extensive-expression purchase-and-hold bank portfolio.

Tiny- and Mid-Cap Lender Sector Valuation Background

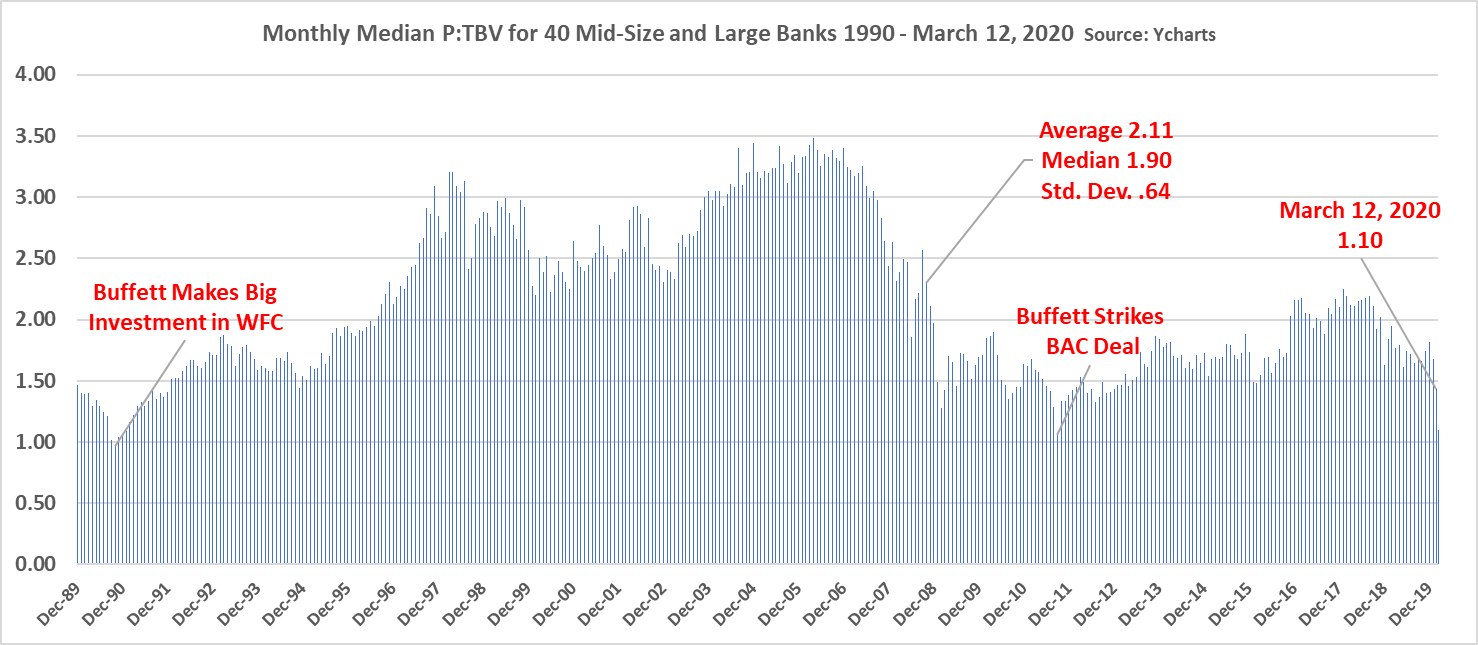

Let me commence by revisiting an posting I posted on Searching for Alpha on March 18, 2020: “12 Charts: The Case for Buffett Obtaining Financial institution Stocks at Present day Valuations.”

The short article revealed twelve amazing charts that every severe financial institution trader demands to know. Below are two charts drawn from the posting.

This one particular demonstrates the median Value to Tangible E book Benefit by thirty day period for 40 US Huge- and Mid-Cap banks from 1990 to 2020. The message at the time was obvious: Banks ended up low-cost in March 2020 at a median P/TBV of 1.10x. That explained, banking companies were being low cost for a purpose: COVID fears. As my poker close friends say, no guts no glory.

Median PE Ratios 40 Financial institutions (YCharts)

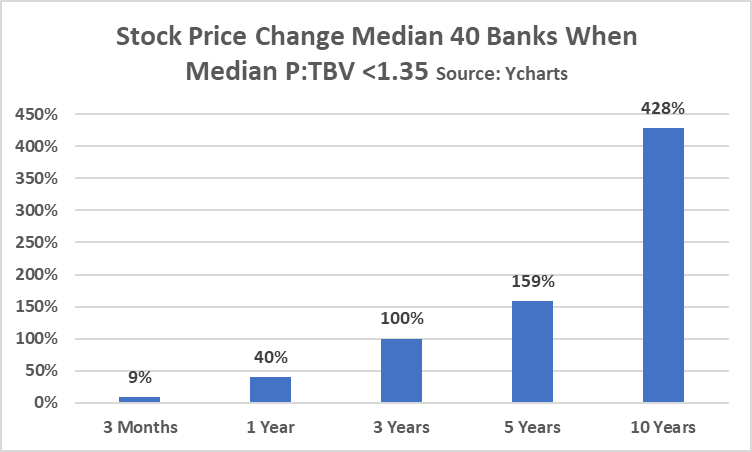

Below is yet another chart from the write-up. This 1 displays the average median cost transform around a variety of timeframes when Massive- and Mid-Cap financial institutions are cheap:

Price Adjust <1.35 P/TBV (YCharts)

Today banks are not as cheap as back in March 2020, but Small- and Mid-Cap banks appear attractively valued for long-term buy-and-hold investors like me.

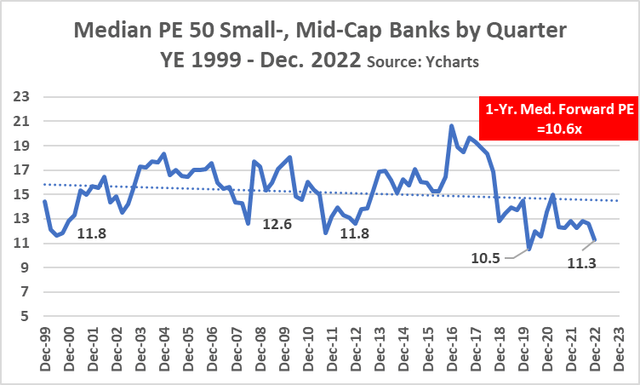

This next chart examines the median quarterly PE of 50 Small- and Mid-Cap banks since YE 1999. Over the past 20+ years these banks have had an average median PE of about 15x. Today that median PE is 11.3x.

Even better, the median one-year forward PE for the banks shows a 10.6x PE. Obviously, the forward PE must be taken with a grain of salt, but I like the direction as it tells me investors in some of these banks have a decent margin of safety.

50 Banks’ Median PE (YCharts)

Investors have earned out-sized total returns in the past when buying Small- and Mid-Cap banks at historically low valuations.

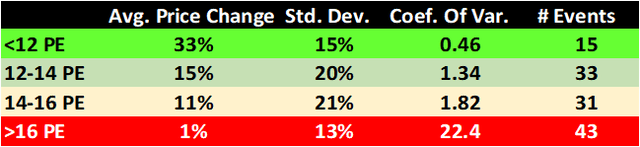

Here are four observations about stock price performance of the 50 Small- and Mid-Cap banks at various PE valuations.

- When the median PE of the banks is less than 12x, historically there has been an average price change of 33{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} one year later. When PEs are greater than 16x, the price returns are on average 1{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9}. (Dividends, of course, provide additional return.)

- Interestingly, as the standard deviation column indicates, one-year stock price variation is lowest at the extremes.

- The third column showing Coefficient of Variance gives investors a sense of risk (variance to the average) the lowest Coefficient of Variance is associated with times when PEs are low, which should not be surprising to long-time investors.

- Finally, a cautionary word: Since YE 1999, there have been only 15 quarters when the median PE for the 50 banks was below 12x as it is today (12/22/2022). The fact that there have been so few events tells us that we cannot consider the data statistically significant. In other words, the data informs our view, but we must be careful to not get overly certain that past is predictive.

Price Return History by PE Ratio (YCharts)

I may post an article in the near future about my current research, but for the remainder of this article, I plan to focus on HBT. While several of the Small- and Mid-Caps banks look attractive today, I find HBT especially attractive for reasons to be described below.

HBT: IPO October 10, 2019/Insider Buy

HBT did an initial public offering on October 10, 2019: 9.4 million shares at $16.00 per share.

The bank is over 100-years old and operates in Central and Northeastern Illinois and Eastern Iowa.

Directors and officers own 65{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} of HBT.

Fred L. Drake serves as Chairman of the Board and CEO, and Chairman of the Board of Heartland Bank. He has been a director of the company since 1984 and a director of Heartland Bank since 1982. He owns 59{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} of HBT.

HBT is a “controlled company,” a term defined by Rule 5615(c) of the Nasdaq Listing Rules. Drake has more than 50{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} of voting power.

I liken HBT’s family-controlled status to that of three banks which I have long respected: Commerce Bancshares Inc (CBSH), First Interstate BancSystem, Inc. (FIBK), and First Citizens BancShares, Inc. (FCNCA). I have owned shares in the first two since at least 2016 and wish I had bought FCNCA back then.

It is worth noting that Fred Drake made two open market buys of HBT in February 2021 at $15.20 (total 3,670 shares).

HBT Key Statistics at a Glance

Source: YCharts, Seeking Alpha, Company 3Q 2022 Press Release

- December 23 closing price: $19.57

- Market Cap: $562 million

- Share count: 28.75 million

- One month price: -3.2{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9}

- YTD price: +8.1{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9}

- One year price: +8.5{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9}

- YTD price range: $16.09-$22.48

- Analyst one-year price target $22.88. (5 analysts, 1 Buy, 1 Outperform, 2 Holds, 1 Underperform, Consensus 2.6, Price Targets: $19.00 – $26.00).

- P/E: 9.9x

- Forward P/E: 9.6x

- Loan/Deposit Ratio: 70{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9}

- Return on Equity Q3: 16.5{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9}. (79th percentile publicly traded banks)

- ROA Q3: 1.47{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} (83rd percentile)

- Cost of Funds Q3: 7 basis points Q3 (95th percentile)

- Net Interest Margin Q3: 365 basis points, +47 BP Y/Y

- Efficiency Ratio Q3: .52 (85th percentile)

- Dividend yield: 3.27{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9}

- Payout Ratio: 32{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9}.

- Beta (3-year): .95

Why I Like HBT for My Long-Term Buy-and Hold Portfolio

Profitability

My chief interest in HBT is it’s generating reliable profitability exceeding the bank’s cost of capital. Though the company only went public in 4Q 2019, FDIC data for HBT’s bank sub, Heartland Bank & Trust, goes back to 2003.

Heartland Bank’s rolling four quarter ROE has averaged 18{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} and ROA 1.9{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} since 2003.

By my calculations, the bank’s Risk-Adjusted Return on Equity (RAROE) since 2003 is ~12{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} and roughly the same over the past decade. (RAROE calculation: Average ROE – Standard Deviation of ROE.)

HBT’s superior RAROE places it among the nation’s elite banks that I hold as long-term investments.

Management

I like being a small owner of a bank that is controlled by a seasoned banker with a long history of superior performance. The board has deep industry experience and local market knowledge.

A risk that is not addressed in HBT’s recent 10-K is succession planning. It is unclear how the board will/would respond if Mr. Drake is not in a position to oversee the bank.

In November, HBT announced several executive management changes. It is unclear if these changes address my concerns about successors to Mr. Drake.

Low Cost of Funds/Strong Core Deposits

At 7 basis points in Q3, HBT is among the nation’s lowest cost producers of funding. This is a huge competitive advantage for the bank in a time of rising rates.

The bank’s most recent 10Q indicates rising rates will further benefit the bank’s net interest margin as follows.

+400 bp = +10.8{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} NII year one, 16.9{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} year two.

+200 bp = 5.9{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} year one, 9.6{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} year two.

+100 bp = 3.0{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} year one, 5.1{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} year two.

Liquidity/Moderate Loan to Deposit Ratio

I like the current loan to deposit ratio at 70{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9}. It’s been as high as 80{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9}, a ratio I consider at the top end of my risk tolerance. The bank has a pending merger that will put moderate upward pressure on the loan to deposit ratio.

Rising rates, while likely favorable to net interest income, could be a double-edged sword should rates rise so high as to put pressure on deposit retention. This risk is most pronounced among “Have Not” banks. As a “Have” bank, however, HBT is not insulated from this risk.

Credit Quality

HBT meets my criteria for being a high-quality lender. According to FDIC data, the bank has had net charge-offs of $79 million since 2003, $30.6 million over the past ten years, and $6.4 million in the past five years. My rough calculation shows the bank’s rolling net charge-offs ratio to be .10{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9}, a number I consider superior for the industry.

That said, the bank took more losses from Q2 2009 to Q2 2011 than I would like to see from a superior lender. My guess is that the board has gone to school on those losses. Since then, the bank has cut back exposure to 1-4 Family from 20{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} in 2010 to 10{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} in the 3Q 2022 quarter.

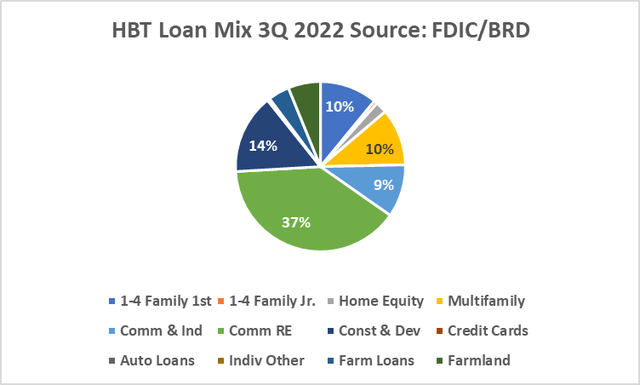

Loan Mix

I like the loan mix. The bank does not show egregious concentrations.

The bulk of HBT’s credit exposure is commercial (70{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} = CRE, C&I, Multi-fam, and C&D). Ten percent is farm-related lending, a number I like a lot since it is one of the highest ratios among publicly traded banks. I like the low exposure to 1-4 Family (10{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9}), a loan category I avoid given its commodity pricing and awful cyclical peaks and valleys banks engaged in heavy 1-4 Family lending rarely earned back their cost of capital over economic cycles.

The watch item for regulators is commercial real estate at 37{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} of loans, up from 26{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} in 2010. I am comfortable with such a high exposure when community banks have a long history of superior credit management.

Loan Mix HBT (FDIC, BRD)

Buybacks/Controlling Shareholder

HBT buys back shares.

HBT has announced three repurchase authorizations since 2020:

In 4Q 2021, the bank 147,383 shares at an average price of $17.52. Total repurchases: $4.9 million.

10-Qs for the first three quarters of 2022 show the following repurchase activity:

Q1 50,062 shares @ $18.84

Q2 136,746 @ $17.61/share

Q3 78,571 shares @ $18.22/share

Repurchase Facts:

- The recent 10-Q indicates HBT has $10.2 million remaining under the current repurchase program.

- Quarterly range in prices paid for repurchases: $17.61 – $18.84.

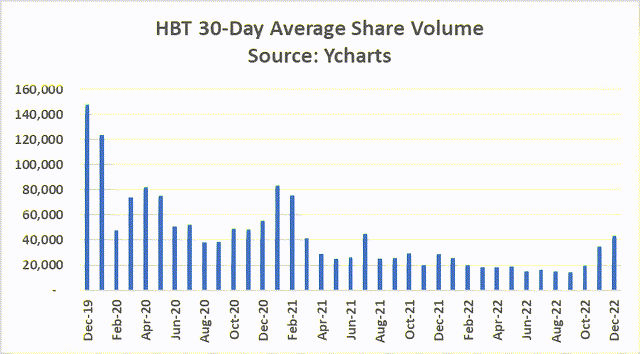

My best guess is that the spike in share trade volume in November and December is associated with accelerated buybacks as the most recent $15 million repurchase authorization expires 12/31/2022. The run-up in stock price during the past two months is likely tied to the surge in buybacks. I would not be surprised to see the stock price decline once buybacks slow which I presume will not pick back up until sometime in 1Q.

A clear benefit of a controlled-interest bank is that the bank’s controlling shareholder (Mr. Drake) will not buy back shares when share prices are too high. In effect, the controlling shareholder acts in a manner similar to Warren Buffett who has long made it known that he will only buy Berkshire shares when valuations warrant.

Share Vol. (YCharts)

Accretive Acquisitions

I have a simple rule of thumb: Avoid banks engaged in big mergers. My definition of “big” is any merger where the acquired bank is more than 50{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} of the asset size of the acquirer. I have extensive data showing such mergers consistently struggle short-term (3 years) with revenue retention and creation.

Small, tack-on mergers can often make sense for banks that operate with a clear profit mindset. Small, tack-on mergers done for “strategic” or “political” reasons often do not make economic sense.

Rural market banks, and even large urban market community banks for that matter, often struggle developing successors to family-controlled banks. A principal driver behind bank sales is the CEO’s recognition that an able successor does not exist. Consequently, a sale is needed to create a liquidity event for shareholders.

HBT has been, and should continue to be, in a position to benefit from this M&A trend in rural markets. Ideally, sellers see HBT, now that the bank is publicly traded, as an attractive buyer who can provide not only cash but equity for sellers.

In October 2021, HBT announced the acquisition of Iowa’s $238 million NXT Bancorporation. Like many banks its size, NXT’s profitability underperformed larger banks. While it showed decent credit quality, NXT suffered from high efficiency ratio associated with lack of scale and asset price pressures.

In August 2022, HBT announced a merger with Springfield, IL bank, $894 million Town and Country Financial Corporation (OTCPK:TWCF). This merger has all the earmarks of a successful merger:

- Drake and HBT are experienced acquirers.

- At the time of the acquisition, HBT indicated that the board expects the merger to be accretive in year one. Per the press release: “Strong EPS accretion of 17{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} expected in 2023 (excluding transaction expenses, assuming transaction closes in first quarter of 2023).”

- TWCF is about 20{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} the size of HBT.

- It operates in central Illinois, a market HBT knows well.

- I like TWCF’s credit history and cost of funds.

- TWCF has a long history of decent but not outstanding profitability (Risk-adjusted Return on Equity of ~5{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} which is less than the bank’s cost of capital.

- Efficiency is about average for banks of its size ($894 million), suggesting HBT has room for prudent expense cuts and revenue enhancement.

- Big positive: TWCF has attractive cost of funds suggesting strong core deposits.

It would be helpful if the press release provided more insight into HBT’s expected transaction expenses. Absent such data, it is difficult to understand payback. I am sure such insight is available to existing shareholders who will get M&A documentation in order to vote for the merger.

Geography

HBT provides exposure to rural and smaller urban markets in Illinois and Iowa, two states in which I have no investment exposure at the present time.

HBT has about one-third of its deposits and loans in Chicago. Not a lot of data is available in the 10-K as to the nature of these assets and liabilities. As I document in my 2016 book, “Investing in Banks,” Chicago together with Los Angeles and New York City, are the three least profitable markets int the country for community banks. My research shows that the low profitability stems from two factors:

- Big banks crowd out small banks in deposit-gathering.

- To attract loans, small banks tend to compete in higher risk commercial real estate, as well as the highly competitive, low-margin commodity 1-4 family lending.

Valuation Comparisons

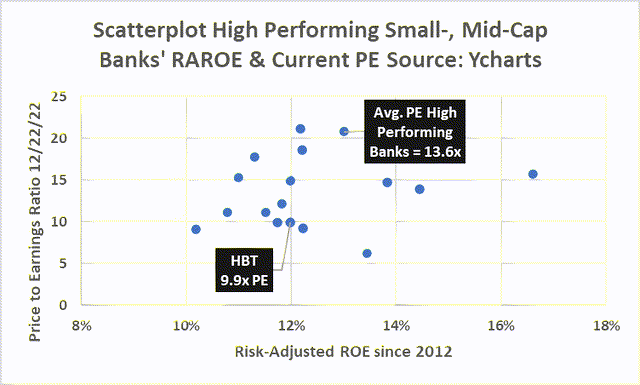

The scatterplot below compares HBT’s current Price to Earnings ratio to PEs of other Small- and Mid-Cap banks with superior Risk-Adjusted Returns on Equity.

What stands out is that the group’s average PE is 13.6x, a ratio about 36{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} higher than that of HBT as of December 22, 2022. On this basis, a case can be made for HBT’s shares to be priced today at ~$26.50.

I could go further and suggest that HBT’s RAROE and history of making accretive acquisitions justify comparisons to four other small-cap banks I respect, each with ~12{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} RAROE:

- Stock Yards Bancorp Inc (SYBT) in Kentucky 21.0x PE

- Lakeland Financial Corp (LKFN) in Indiana 18.5x PE

- City Holding Co (CHCO) in West Virginia 14.9x PE

- Arrow Financial Corp (AROW) in New York 12.1x PE

The average PE of this elite group of banks is ~16.5x. A 16.5x PE for HBT moves the bank’s stock price to ~$32. While I do not think a $30+ price is likely in 2023, assuming credit quality remains sound, getting to $30 appears reasonable in 2024-2025.

PE Ratios High Quality Banks (YCharts)

Final Thoughts: Value Creation Catalysts

I see HBT having several catalysts for value creation:

- Rising rates improve NII

- Buybacks provide margin of safety

- Accretive acquisition in 2023

- Valuation “normalization” to top peers.

- Improving valuations for the sector.

Shares I have acquired to date have been at prices between $17.80 and $19.50. I will continue to acquire HBT shares ambitiously <$20 and selectively <$23.

Risks that stand out for HBT:

- Illinois as a state has a long history of uneven banking performance though it seems that problem banks have been eliminated, only a deep recession will reveal the truth.

- Illinois is a tough state to do business in today given high corporate taxes and the constant battle between rural/small urban markets and Chicago (HBT has current tax rate of 26.5{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} which is higher than most US community banks) Illinois’s pension gaps and financial challenges are so significant that the state could raise taxes further on companies and individuals, jeopardizing jobs and local economies.

- While rising interest rates can help HBT, if rates rise too high, borrowers could struggle repaying loans.

- As with all banks, a deep recession could require HBT to significantly increase Provision expense.

- I remain interested in learning more about the bank’s CEO succession plan.

- A bank like HBT depends significantly on third party processors like Fidelity National Information Services Inc (FIS), Fiserv, Inc. (FISV), and Jack Henry & Associates, Inc. (JKHY). Adversity facing these processors (e.g., cyber) is a direct risk to HBT and other community banks.

- Liquidity (ability to sell HBT shares) is a concern given the thin market cap and low trading volume.

- Liquidity concerns are exacerbated by the risk that the controlling shareholder (or successors) could need or desire to raise cash by selling shares and reducing bank investment exposure investors in First Interstate saw this risk play out over the past two years.

In recognition of these risks, I do not see HBT becoming a top five holding in my long-term buy-and-hold portfolio bank portfolio.

My goal for the portfolio is to continue to hold a well-diversified (geography, credit, business models, customer segments) group of high-quality banks. Banks currently in this portfolio are:

Readers can find my most recent articles on these banks by going to the link highlighted in the bank name.

Caveat

The foregoing is my opinion which I share for the purpose of getting feedback and questions that challenge my ideas and assumptions.

Every investor needs to do his/her own due diligence before investing as well as determine their risk profile. I am risk-averse, preferring to invest in the nation’s best banks which reliably earn returns exceeding cost of capital.

Editor’s Note: This article was submitted as part of Seeking Alpha’s Top 2023 Pick competition, which runs through December 25. This competition is open to all users and contributors click here to find out more and submit your article today!