Revisiting Ameriprise Financial: Now A ‘Hold’ For 2023 (Rating Downgrade) (NYSE:AMP)

J. Michael Jones

Dear followers/readers,

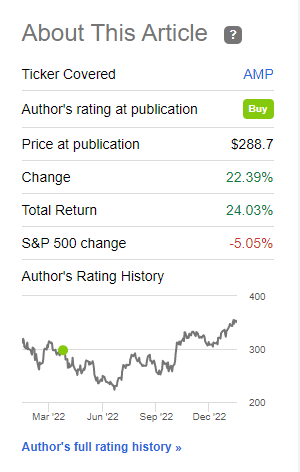

Ameriprise Financial, Inc. (NYSE:AMP) has been one of those successful stocks/companies that I had introduced to me several years ago. Since forecasting and finding what sort of seems to work for this company, I’ve never really looked back, and always keep either a watchlist or a significant position of the company in my portfolio. The current position is around 1{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9}, and it’s about 10 months old from my last article back in April of 2022. Back then, I went back to a “BUY” and positive. This has turned out to be exactly the right thing to do, with the following results since publication and increasing my stake.

Seeking Alpha Ameriprise (Seeking Alpha)

This sort of investing is a big part of why my returns outperform the broader average, and why I’m up in a year where most indexes were down double digits. I know my quality companies, and I buy them cheap – Ameriprise is one of them.

Let’s revisit the company for 2023 and see what we have.

Ameriprise Financial for 2023

I’ve mentioned before what a great business Ameriprise is – so, no introductions or significant charting here. The company is a significant player in integrated asset management, retirement, and ancillary wealth management services, both on a national as well as a global scale.

It’s mostly wealth management (“WM”) at this point, which makes it somewhat rare to some peers. WM drives over 80{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} of the company’s annual revenues, and it has very long-term client relationships with individuals and organizations that trust Ameriprise’s capacities in ways only possible through decades of building valuable relationships.

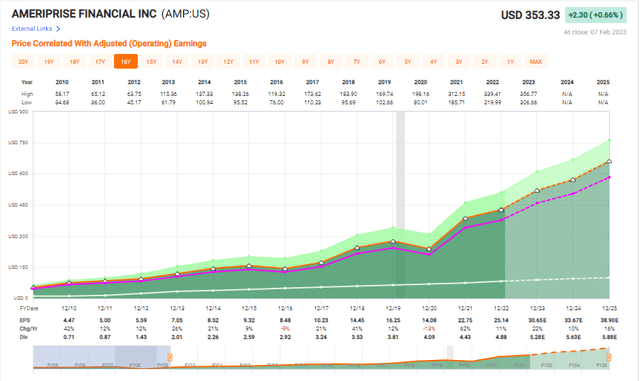

The company has impressive, internal synergies from one set of operations to another, which drives sales in one segment to sales in another. This results in impressive free cash flow generation, which is why the company boasts an EPS chart such as this over time.

Ameriprise financial earnings (F.A.S.T graphs)

Remember, when in doubt, go to math. The market valuations don’t really tell the story of how the company has been doing – financial reporting and filings do that. The market just reacts. And the fact is that while AMP has been able to, as you see above, deliver mostly unfailing growth for almost 15 years, the fact is the share price has gone both up and down in the meantime – but the underlying operations are very solid, and this is the primary reason I am an investor.

If something concerns wealth management, retirement, or asset solutions, Ameriprise tends to offer it – and its quality is confirmed through a 50{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9}+ typical operating RoE.

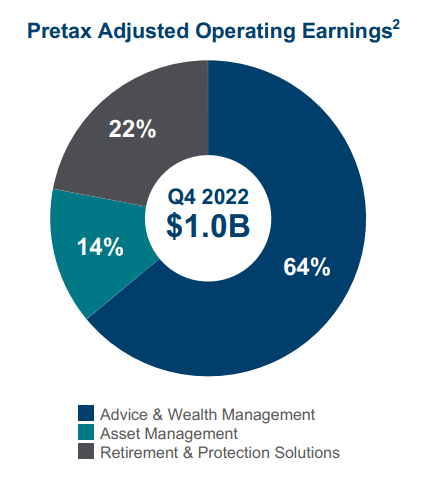

The latest results do little to dispel this upside or notion of quality. We have 4Q22 results that came in less than 2 weeks ago, and despite declines from a strong comparison period, the company remains solid. EPS is up 13{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} for the quarter, and 11{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} for the year, excluding unlocking impacts.

The company’s earnings in wealth management continue to drive results, and grew by 41{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} in 4Q22, driving 64{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} of company EPS. The reason for this solid growth was both fundamentals, as well as growth from the relatively new Ameriprise Bank. The asset management segment is seeing market challenges from how things are currently playing out, but is attempting to compensate through expense management.

Meanwhile, the remainder of the company is delivering results, and also is showing the lower overall risk profile I’ve been expecting, which compared to other insurers, puts the company in an extremely advantageous position in terms of risk management that insulates it from crashes that have happened not only to Unum (UNM), but Lincoln National (LNC) as well, two companies I’ve invested in in the past. It’s, of course, impossible to completely cover or protect oneself here, but the company has done well to position its portfolio and assets with this in mind.

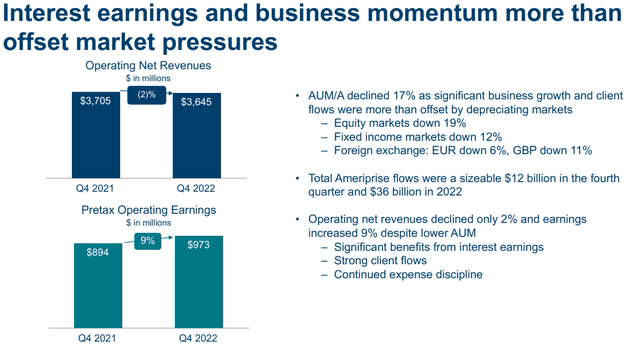

AMP IR (AMP IR)

The way these companies work is quite interesting. While Ameriprise Financial, Inc. is obviously seeing market pressures from poor overall market performance (at least until January, we’ll see how the recent surge impacts things, of course), it’s important to remember that the company has correlative exposure to interest rates movement – in that increases in interest rates also mean positive earnings for AMP stock. In this case, any movement and business results completely negated the impacts of the market and more besides.

AMP Ir (AMP Ir)

This is what we want to see from virtually all insurers, but something we rarely see as clearly as we do here. Wealth management, even though client assets are down from record-driven $858B in 2021 to $758B in 2022, is still not a problem, because client flows and TTM revenue on a per-advisor basis, are actually up.

So the company, despite lower assets under management (“AUM”), is doing very well – and delivering record margins of 30{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} and above. While not 100{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} class-leading, it’s getting there. The growth in the banking segment for AMP will further drive earnings, as the interest rate correlation rises.

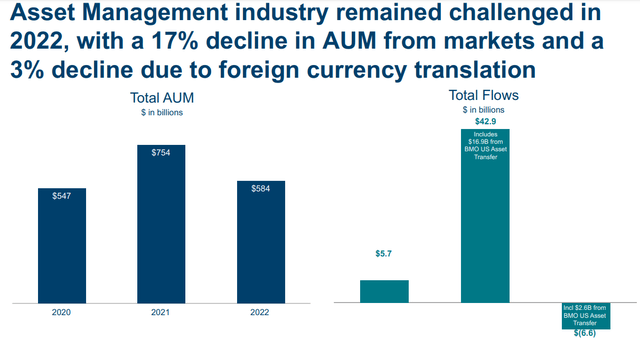

Asset management is really the only black sheep in the bunch – both negative FX due to the dollar, and the market as well as the impacts in AUM in the sector are quite impaired here, and flows are actually negative for the year.

AMP IR (AMP IR)

We’re likely to see a reversion or a break here in 1Q23, due to the market correlation of this segment, but it’s also important to not underestimate the cost structures and expense impacts found in these segments. Asset management is a sort of segment in which when the market turns sour – it all turns sour. Asset flows go down, equity and fixed market depreciation are impacted, and mark-to-market adjustments cause negative impacts together with the impacts in performance fees. AMP saw a stable fee rate at 48 bps, but it still went down in terms of fees overall by $30M YoY. Margins in this segment were below 30{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} for the quarter.

But this is really only a minor point in a quarter otherwise highlighted by positive development across most fields. The retirement solutions segment saw an increase in earnings due to enhanced fixed yields, lower amortization, and continued optimization. The company’s RBC remains at 530{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9}+, which is among the leading in the entire industry.

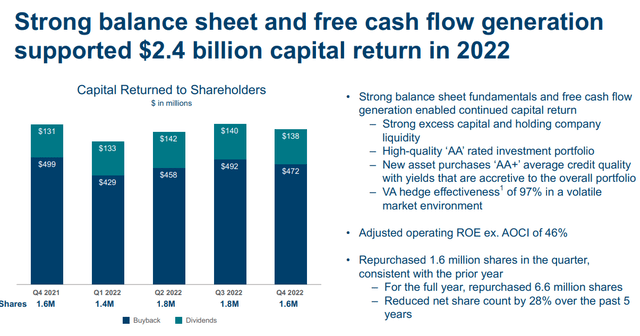

Also, AMP’s balance sheet remains titanium-grade, as you can see below.

AMP IR (AMP IR)

So how exactly does this influence the appeal and investability of AMP? Why am I, as you can see, moving to a “HOLD” stance for a company that seems to be doing so well?

For a very simple reason.

Ameriprise – A qualitative valuation play above all, and valuations say “HOLD”

Ameriprise Financial stock remains above all, a valuation-oriented play. If you take a look at the 10-year trend, with share price back on the table and normalized discount back as well, you’ll see that there are times to “BUY” and times to “SELL” or trim the company position. The normalized discount level gives us a very good idea of where this is possible.

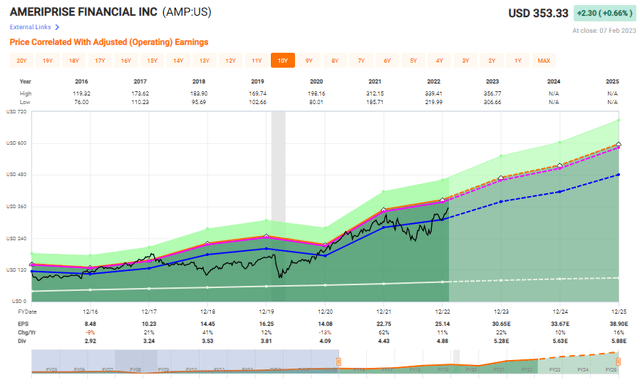

Ameriprise Valuation (AMP F.A.S.T graphs)

Don’t get me wrong. As you can see, you could have held the company throughout all the dips and so forth, and likely still come out on top in the long term. That’s the key to a qualitative company. However, my investment strategy includes trimming and selling at high valuations and investing in lower-valued companies for higher upsides. So, while I’ve actually made triple digits with AMP, I’ve made even more long-term by doing this strategically over time.

AMP goes up and down – and the time to buy it, I would say, is below a 12.5x P/E. This is a good baseline where the company is below, it’s a fairly good indicator for a typical 2{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9}+ yield, and a double-digit upside that’s over 10-15{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9}. Above that, and above 13x, the company’s upside typically dips down to around 10-12{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} at most, and much of that is predicated on a growth estimate that has been known to deliver dips.

I said in my previous article, that the forecasted growth by AMP here is excellent. This is still true – but it’s also all about that valuation. At current estimates and valuation, the upside here is no longer 15-25{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9}, it’s 8-12{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} annually. While this may be good enough for some, remember that this comes with a low yield of 1.42{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} in a typically high-yielding sector of finance, asset management, and custody banks. If we look at the peer group and start to include banks that are relevant due to the AMP bank, we can easily find yields that by themselves are higher than the lower-range upside here on an annual basis.

This is a bit of a problem for me – because what’s available in virtually any other undervalued financial company here is far better. Yes, AMP is one of the best-rated ones at an A-rating here.

Still, there is a lot to like about Ameriprise Financial. That’s what drew me to investing in the business in the first place after all and that’s why, despite having sold some of my shares at a high valuation, I still have some of my position in the company left as I’m writing this article – but with the very clear intention of rotating them into lower-valued assets and companies to maximize the upside potential I have here.

Looking at analyst forecasts and valuations, S&P Global calls the company a “BUY,” but only with a 3.5{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} upside to an average PT of around $365, from a range of $287 and $430 at the highest. Remember, analysts here have the unfortunate tendency to overshoot quite a bit once this company goes into positive territory. My own PT as of my last article was $305 – that was the midpoint 12.5-12.6x P/E.

As of this article, I’m bumping that target to update for new forecasts – the new 12.5x AMP target is around $335, $340 at most. I’m not going any higher than that, and the company is currently trading close to $350/share.

You can guesstimate where this ends up going in terms of thesis – but I’ll also mention here that forecasts aren’t as perfect as we’d like, with around 20{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} negative miss ratio on a 10-year basis, even with a 10{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} margin of error.

When this company reaches a lower valuation, it becomes one of my highest-conviction quality “BUYs.”

But in this specific situation, I view Ameriprise Financial, Inc. as likely to potentially underperform. If we see a similar downturn we’ve seen many times before, the short-term potential is for AMP to generate a negative RoR of around 4-7{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} in 2023, should it normalize towards an 11-12x P/E during this year.

That is why I’m changing my stance here.

Thesis

My thesis for Ameriprise Financial, Inc. is the following:

- This is an excellent company provided you can buy AMP at a conservative 12.5X 2022E midpoint P/E – the annualized RoR at such a scenario is over 15{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9}, and this would be buy-worthy.

- Today however, forecasts are different, and we’re looking at 8-12{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} based on current 13x+ P/E valuations, which causes me to change my rating on AMP and proceed with trimming my position in the company. My PT for AMP as of 2023 is $335/share.

- I consider AMP a “HOLD.”

Remember, I’m all about:

- Buying undervalued – even if that undervaluation is slight and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn’t go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company, therefore, does not fulfill my valuation-related criteria, which dictates “HOLD” here.