Here’s How 4 Dow Finance Stocks are Holding Up in Bear Market

The Dow Jones Industrial Average Index has slipped into the bear market. Following yesterday’s decline of 1.1{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9}, the index is now down 20.5{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} from its Jan 4 peak (hence meeting the definition of a bear market).

Worries that the Federal Reserve’s aggressive stance to fight decade-high inflation will push the U.S. economy into a downturn have weighed on investor sentiments since the beginning of 2022. This has sent the domestic equity markets tumbling after a solid performance last year.

The Dow, the 30-stock blue-chip index, rallied almost 19{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} in 2021. But macroeconomic and geopolitical concerns have led to a pessimistic stance since the start of this year. Today we are looking into the performance of four financial services stocks – JPMorgan JPM, Goldman Sachs GS, Visa V and American Express AXP – that are part of the index.

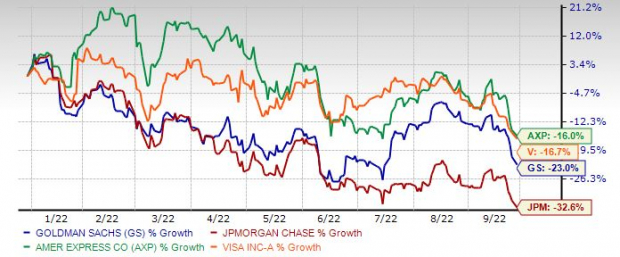

So far this year, shares of JPM, GS, V and AXP have plunged 32.6{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9}, 23{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9}, 16.7{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} and 16{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9}, respectively. The beaten-down stock prices might turn out to be an attractive entry point for investors in quality franchises.

Year-to-Date Price Performance

Image Source: Zacks Investment Research

While the central bank’s efforts to curb inflation by raising interest rates will benefit the finance sector stocks, the expectations of economic slowdown/recession in the coming six-nine months remain a big headwind. Until now, consumer confidence and spending are holding up well, but with the steady rate increase, these are likely to witness weakness.

Hence, investors are shying away from stock markets. Nonetheless, this is the best time to invest in quality stocks that are fundamentally strong and will bounce back resoundingly once these concerns go away.

Let’s now discuss the above-mentioned four Dow finance stocks in detail.

JPMorgan is the largest bank (in terms of consolidated assets and market cap) in the United States. The company is a bellwether in the banking space, given the sheer size (serves more than 66 million U.S. households) and quality of its asset base and industry-leading franchises in investment, commercial and consumer banking businesses.

JPM’s balance sheet is highly asset-sensitive, and rising rates will support top-line growth. The company has been extensively investing in technology to stay ahead of the competitors, which include not only other banks but also technology firms. The company has been growing through on-bolt acquisitions, which will strengthen its operations through technological advancement.

After consolidating its branch network for several years, this Zacks Rank #3 (Hold) company announced an initiative in 2018 to expand in new regions by opening branches. This bodes well in garnering market share and offers solid cross-selling opportunities in the card and auto loan sectors. It is also expanding operations overseas, in China and Europe.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Despite a challenging operating environment, JPM’s deposits and loan balances have remained strong. Though loan demand has been subdued since the onset of the coronavirus pandemic in 2020, there has been a marked improvement in the same of late. In the six months ended Jun 30, 2022, total loans grew 6{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} year over year to $1.1 trillion.

While higher rates and the expected global economic slowdown will continue hampering investment banking (IB) business, JPMorgan’s leading position in garnering global IB fees will offer leverage. Also, ongoing macroeconomic concerns and geopolitical tensions should keep the markets volatile in the quarters ahead, helping the company earn measurable trading revenues (which account for almost 25{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} of its total net revenues).

Also, JPM currently pays investors $4.00 per share as an annual dividend, which yields 3.66{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9}. The company increased its dividend four times in the past five years, and its payout grew 14.82{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} over the same time period. JPM’s payout ratio is 32{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} of earnings at present.

The Zacks Consensus Estimate for 2022 and 2023 has moved slightly north over the past week.

Goldman, one of the major players in IB business, is undertaking measures to diversify operations. The company is making efforts inorganically to boost asset management and wealth management businesses, while expanding its digital consumer banking platform – Marcus by Goldman Sachs.

In April 2022, this Zacks Rank #3 company acquired Dutch asset manager NN Investment Partners, while in March, it closed the acquisition of GreenSky. In 2020 and 2019, it completed the purchase of Folio Financial and United Capital, respectively. Further, its asset management division has announced a deal to acquire robo-advisor NextCapital.

The company’s IB revenues, which witnessed a four-year CAGR of 22.1{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} (ended 2021), fell in the first half of 2022 due to a decline in industry-wide completed M&A transactions. Yet, Goldman’s solid position in worldwide announced and completed M&As will likely give it an edge over its peers. Robust client engagement, backed by digital disruption and transformation trends, and its decent investment banking backlog are other tailwinds.

Backed by a solid capital position, Goldman has consistently enhanced shareholders’ value. Following the clearance of the 2022 stress test, the company announced an increase in the quarterly dividend by 25{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} to $2.50 per share in July. Prior to this, it announced a dividend hike by 60{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} to $2 per share last year.

Based on the dividend paid out over the trailing four quarters, GS has a dividend yield of 3.31{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9}. In the last five years, the company has increased its dividend five times, with an annualized growth rate of 25.7{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9}. Further, the company’s payout ratio is 18{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} of earnings.

Also, GS looks undervalued with respect to price-to-earnings (P/E) and price-to-book (P/B) ratios. The stock has a P/E (F1) ratio of 8.66, which is lower than the industry average of 12.45. Also, its P/B ratio of 0.96 is below the industry average of 1.54.

Over the past week, the Zacks Consensus Estimate for 2022 and 2023 has remained unchanged.

Visa operates as a payments technology company globally. In recent years, the company has evolved its business to accelerate the migration of digital payments across new channels. It has also adopted new digital payment and security technologies, such as contactless and tokenization.

Visa Token Service, Visa Checkout and Visa In-App Provisioning are some of the digital solutions that have been developed by the company to advance its digital platform. V is also pushing technologies, including contactless and scan-to-pay, tap-to-pay, and secure remote commerce, which should be the main modes of payment in the near future. Thus, Visa has significant prospects for growth in the emerging payments industry in the years to come. It is well poised for growth owing to BNPL, crypto and other fintechs.

For Visa, M&As, partnerships and minority investments are some of the ways to achieve robust growth. These moves have helped the company to maintain its leading position in the payment network space. It consistently made efforts to expand its presence in Latin America, South Africa and Europe.

This Zacks Rank #2 (Buy) company has been witnessing tremendous revenue growth on the back of expanded payments volume and the number of processed. The trend will continue, driven by its strong market position and an attractive core business supported by new deals, renewed agreements, accretive acquisitions, increasing spending via cards, shift to the digital form of payments and expansion of service offerings.

V enjoys compelling cash and available-for-sale investment position along with a healthy free cash flow, which enables it to make acquisitions and fund capital expenditure. Backed by its strong cash position, it remains committed to boosting shareholders’ value. Visa has increased its dividend each year since 2009, with the latest being a 17{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} hike in October 2021 to 37.5 cents per share. The stock has a five-year annualized dividend growth of 16.6{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9}. Further, the payout ratio of V is 21{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} of earnings at present.

The Zacks Consensus Estimate for 2022 has moved marginally upward, while that for 2023 has remained unchanged over the past seven days.

American Express, one of the leading providers of credit payment card products, is expected to witness a solid revenue rise driven by several growth initiatives, such as launching products, enhancing the existing features, modifying prices, reaching agreements and forging alliances, among others. Even though the COVID-led fall in business volumes hampered its top line in 2020, the same has been picking up gradually on rebounding economic growth and increasing consumer spending.

With its new growth plan, AXP anticipates gaining solidly from the improving macro environment. Rising credit card spending will boost its future performance. Management expects revenues to increase 23-25{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} this year, with the target to achieve growth of more than 10{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} over the long term.

This Zacks Rank #2 company is working to provide digitized services to its customers. It has acquired a number of digital companies in the past, which along with new digital features and content that American Express is building in-house, will enable its card members to engage more and thus, drive card usage volumes and revenues.

Further, American Express made a significant move in small business banking by acquiring Kabbage, an online lender, in 2020. Since then, the company has been expanding the services offered by Kabbage, which will help rapidly grow its business in the domestic market and diversify revenue sources. The company also forms strategic partnerships with Delta, Hilton and Amazon. It recently announced a new financial advice service with Vanguard.

The company has robust cash-generating abilities in place through which business investment and prudent shareholder-friendly moves are undertaken. This March, the company announced a hike of around 20{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} in the quarterly dividend to 52 cents per share. The company has a dividend yield of 1.48{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} and five-year annualized dividend growth of 7.2{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9}. Further, AXP’s payout ratio is 21{d0229a57248bc83f80dcf53d285ae037b39e8d57980e4e23347103bb2289e3f9} of earnings at present.

Also, American Express currently has a Value Score of B. Our research shows that stocks with a Value Score of A or B, when combined with a Zacks Rank #1 or 2, offer the best upside potential.

The Zacks Consensus Estimate for 2022 and 2023 has remained unchanged over the past seven days.

Just Released: Zacks Unveils the Top 5 EV Stocks for 2022

For several months now, electric vehicles have been disrupting the $82 billion automotive industry. And that disruption is only getting bigger thanks to sky-high gas prices. Even titans in the financial industry including George Soros, Jeff Bezos, and Ray Dalio have invested in this unstoppable wave. You don’t want to be sitting on your hands while EV stocks break out and climb to new highs. In a new free report, Zacks is revealing the top 5 EV stocks for investors. Next year, don’t look back on today wishing you had taken advantage of this opportunity.>>Send me my free report revealing the top 5 EV stocks

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

The Goldman Sachs Group, Inc. (GS): Free Stock Analysis Report

JPMorgan Chase & Co. (JPM): Free Stock Analysis Report

Visa Inc. (V): Free Stock Analysis Report

American Express Company (AXP): Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.